UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL

YEAR ENDED

Commission

file No.

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (I.R.S. Employer Identification No.) | |

| incorporation or organization) | ||

| (Address of principal executive offices) | (Zip Code) |

Registrant’s

telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The |

Securities registered pursuant to section 12(g) of the Act: None.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

o

Indicate

by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant

to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and emerging growth company in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | o | |

| Non-accelerated filer | o | Smaller reporting company | |

| Emerging growth company | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes x No o

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

o

The aggregate

market value of Rollins, Inc. Common Stock held by non-affiliates on June 30, 2020 was $

Rollins, Inc. had shares of Common Stock outstanding as of January 31, 2021.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2021 Annual Meeting of Stockholders of Rollins, Inc. are incorporated by reference into Part III, Items 10-14.

Rollins, Inc.

Form 10-K

For the Year Ended December 31, 2020

Table of Contents

| 2 |

PART I

| Item 1. | Business |

General

Rollins, Inc. (the “Company”) is an international service company with headquarters located in Atlanta, Georgia, providing pest and termite control services through its wholly-owned subsidiaries and independent franchises to both residential and commercial customers in the United States, Canada, Australia, Europe, and Asia with international franchises in Canada, Central and South America, the Caribbean, Europe, the Middle East, Asia, Africa, and Australia. Our pest and termite control services are performed through a contract that specifies the pricing arrangement with the customer.

For a listing of the Company’s Subsidiaries, see Note 1 - Summary of Significant Accounting Policies in the Notes to the Financial Statements (Part II, Item 8, of this Form 10-K).

The Company has one reportable segment, its pest and termite control business. Revenue, operating profit and identifiable assets for this segment, which includes the United States, Canada, Central and South America, the Caribbean, Europe, the Middle East, Asia, Africa, and Australia are included in Item 8 of this document, “Financial Statements and Supplementary Data” beginning on page 26. The Company’s results of operations and its financial condition are not reliant upon any single customer or a few customers or the Company’s foreign operations.

Three-for-Two Stock Split

All share and per share data presented have been adjusted to account for the three-for-two stock split effective December 10, 2020.

Common Stock Repurchase Program

At the July 24, 2012 Quarterly Board of Directors’ meeting, the Board authorized the purchase of 16.9 million shares of the Company’s common stock. During the years ended December 31, 2020 and 2019, the Company did not repurchase shares on the open market. In total, there are 11.4 million additional shares authorized to be repurchased under prior Board approval. The repurchase program does not have an expiration date.

Franchising Programs

Orkin Franchises

The Company, through its wholly-owned subsidiary Orkin Systems, LLC (“Orkin Systems”), began its domestic Orkin franchise program in the U.S. in 1994, and established its first international franchise in 2000. It has since expanded to Central and South America, the Caribbean, Europe, the Middle East, Asia, and Africa. The Company continues to expand its growth through the franchise program of its Orkin brand. This program is primarily used in smaller markets where it is currently not economically efficient to establish and operate a company-owned Orkin branch. Domestic Orkin franchises are subject to a contractual buyback provision at Orkin System’s option with a pre-determined purchase price using a formula applied to revenues of the franchise. International Orkin franchise agreements also contain an optional buyback provision, but it is subject to the franchisee’s renewal option.

| At December 31, | ||||||||||||

| Orkin franchises | 2020 | 2019 | 2018 | |||||||||

| Domestic franchises | 49 | 50 | 47 | |||||||||

| International franchises | 94 | 97 | 86 | |||||||||

| Total Orkin franchises | 143 | 147 | 133 | |||||||||

| 3 |

Critter Control Franchises

The Company expands its animal control growth through the franchise program of its wholly-owned subsidiary, Critter Control, Inc. (“Critter Control”). The Company has purchased several Critter Control locations from its franchise owners while renaming and converting several previous Trutech, LLC locations to Critter Control locations. The majority of Critter Control’s locations are franchised. Critter Control franchises are subject to a contractual buyback provision at Critter Control’s option with a pre-determined purchase price using a formula applied to revenues of the franchise.

| At December 31, | ||||||||||||

| Critter Control franchises | 2020 | 2019 | 2018 | |||||||||

| Domestic franchises | 79 | 84 | 80 | |||||||||

| International franchises | 0 | 1 | 1 | |||||||||

| Total Critter Control franchises | 79 | 85 | 81 | |||||||||

Australia Franchises

The Company has Australian franchises through Rollins Australia Pty Ltds wholly-owned subsidiaries, Scientific Pest Management (Australia/Pacific) Pty Ltd (“Scientific Pest Management”) and Murray Rollins Pty Ltd (“Murray Pest Control”).

| At December 31, | ||||||||||||

| Australia franchises | 2020 | 2019 | 2018 | |||||||||

| Total Australia franchises | 9 | 10 | 10 | |||||||||

Seasonality

The business of the Company is affected by the seasonal nature of the Company’s pest and termite control services. The increase in pest presence and activity, as well as the metamorphosis of termites in the spring and summer (the occurrence of which is determined by the timing of the change in seasons), has historically resulted in an increase in the revenue of the Company’s pest and termite control operations during such periods as evidenced by the following chart.

| Total Net Revenues | ||||||||||||

| (in thousands) | 2020 | 2019 | 2018 | |||||||||

| First quarter | $ | 487,901 | $ | 429,069 | $ | 408,742 | ||||||

| Second quarter | 553,329 | 523,957 | 480,461 | |||||||||

| Third quarter | 583,698 | 556,466 | 487,739 | |||||||||

| Fourth quarter | 536,292 | 505,985 | 444,623 | |||||||||

| Years ended December 31, | $ | 2,161,220 | $ | 2,015,477 | $ | 1,821,565 | ||||||

Materials and Supplies

The Company has relationships with a national pest control product distributor and other suppliers for pest and termite control treatment products. The Company maintains a sufficient level of chemicals, materials and other supplies to fulfill its immediate servicing needs and to alleviate any potential short-term shortage in availability from its national network of suppliers. Additionally, the Company procured adequate supplies of gloves, masks, sanitization chemicals and other personal protective equipment that were in high demand during the pandemic.

| 4 |

Competition

The Company believes that, through its wholly-owned subsidiaries Orkin, LLC (“Orkin”), Western Industries-North, LLC (“Western Pest Services”), The Industrial Fumigant Company, LLC (“IFC”), HomeTeam Pest Defense, Inc. (“HomeTeam”), Crane Acquisition, Inc. (“Crane Pest Control”), Waltham Services, LLC (“Waltham”), Trutech, LLC (“Trutech”) PermaTreat Pest Control Company, Inc. (“Permatreat”), Critter Control, Northwest Exterminating Co., LLC (“Northwest”), Okolona Pest Control, Inc. (“OPC”), Clark Pest Control of Stockton, Inc. (“Clark Pest Control”), McCall Service NW, LLC (“McCall”), Orkin Canada Corporation (“Orkin Canada”), Critter Control British Columbia, Inc. (“Critter Control Canada”), Allpest Pest Control (“Allpest”), Murray Pest Control, Scientific Pest Management, Statewide Rollins Pty Ltd (“Statewide”), Adams pest Control Pty Ltd (“Adams”), Safeguard Pest Control and Environmental Services Limited (“Safeguard”), AMES Group Limited (“AMES”), Guardian Pest Control Ltd (“Guardian”), Albany Environmental Services Ltd (“Albany”), Van Vynck Environmental Services Ltd (“Van Vynck”), and Aardwolf Pestkare (Singapore) Pte Ltd (“Aardwolf”), it competes favorably with competitors as the world’s largest pest and termite control company. The Company’s major competitors include Terminix, Ecolab, Rentokil and Anticimex.

The principal methods of competition in the Company’s pest and termite control markets are quality of service, customer proximity, guarantee terms, reputation for safety, technical proficiency, and price.

Research and Development

Expenditures by the Company on research activities relating to the development of new products or services are not significant. Some of the new and improved service methods and products are researched, developed and produced by unaffiliated universities and companies. Also, a portion of these methods and products are produced to the specifications provided by the Company.

The Company maintains a close relationship with several universities for research and validation of treatment procedures and material selection.

The Company conducts tests of new products with the specific manufacturers of such products. The Company also works closely with leading scientists, educators, industry consultants and suppliers to improve service protocols and materials.

Environmental and Regulatory Considerations

The Company’s business is subject to various legislative and regulatory enactments including, but not limited to, environmental laws, antitrust laws, employment laws (including wage and hour laws, payroll taxes and anti-discrimination laws), immigration laws, motor vehicle laws and regulations, human health and safety laws, securities laws including, but not limited to, SEC regulations, and federal, state and local laws and regulations governing worker safety and the pest and termite control industry. Compliance with these requirements may have a material effect on the Company’s capital expenditures, earnings, and competitive position.

Environmental, Health and Safety Matters

Specifically, our businesses are subject to various international, federal, state and local laws and regulations regarding environmental, health and safety matters. Among other things, these laws regulate the emission or discharge of materials into the environment, govern the use, storage, treatment, disposal, transportation and management of hazardous substances and wastes and protect the health and safety of our employees. These laws also impose liability for the costs of investigating and remediating, and damages resulting from, present and past releases of hazardous substances, including releases by prior owners or operators of sites we currently own or operate. Compliance with environmental, health and safety laws increases our operating costs, limits or restricts the services we provide and subjects us to the possibility of regulatory or private actions or proceedings.

Consumer Protection, Privacy and Solicitation Matters

Additionally, we are subject to international, federal, state, provincial and local laws and regulations designed to protect consumers generally, including laws governing lending, debt collection and consumer finance, consumer privacy and fraud, the collection and use of consumer data, telemarketing and other forms of solicitation. The telemarketing rules adopted by the Federal Communications Commission pursuant to the Federal Telephone Consumer Protection Act of 1991 and the Federal Telemarketing Sales Rule issued by the Federal Trade Commission govern our telephone sales practices. The CAN-SPAM Act regulates our email solicitations and the Consumer Review Fairness Act regulates consumer opinions on social media regarding our products and services. The California Consumer Privacy Act provides consumers the right to know what personal data we collect, how it is used, and the right to access, delete and opt out of the sale of their personal information to third parties. If we were to fail to comply with any of these applicable laws or regulations, we could be subject to substantial fines or damages, be involved in lawsuits, enforcement actions and other claims by third parties or governmental authorities, suffer losses to our reputation and our business or suffer the loss of licenses or penalties that may affect how the business is operated, which, in turn, could have a material adverse effect on our financial position, results of operations and cash flows.

| 5 |

Franchise Matters

Certain of our subsidiaries are subject to various international, federal, state, provincial and local laws and regulations governing franchise sales, marketing and licensing and franchise trade practices generally, including applicable rules and regulations of the Federal Trade Commission. These laws and regulations generally require disclosure of business information in connection with the sale and licensing of our franchises. Certain state regulations also affect our ability as a franchisor, to revoke or refuse to renew a franchise. From time to time, we and one or more franchisees have, and may in the future become, involved in a dispute regarding the franchise relationship, including payment of royalties or fees, location of branches, advertising, purchase of products by franchisees, non-competition covenants, compliance with our standards or franchise renewal criteria. Any such franchise dispute could have a material adverse effect on our financial position, results of operations and cash flows.

Human Capital

We believe one of the largest contributors to our Company’s success is the quality of our people. Attracting, developing and retaining high-quality talent is the primary objective of our human capital management. The development and retention of high-quality talent leads to a better customer experience and better customer retention. We develop and engage our people through our best-in-class training at all levels of our organization.

As of December 31, 2020, the Company had 15,616 employees. Approximately 14,200 of our employees were located in the United States, with approximately 13,500 employees at U.S. branch offices. Of the U.S. employees, less than 5% are represented by a labor union or covered by a collective bargaining agreement.

| At December 31, | 2020 | 2019 | 2018 | |||||||||

| Employees | 15,616 | 14,952 | 13,734 | |||||||||

Diversity, Equity and Inclusion

We make it a priority to promote and create a diverse, equitable and inclusive workplace that results in higher levels of satisfaction and engagement, stronger staff retention, higher productivity, and a heightened sense of belonging. Our mission is to have a culture of inclusion, where all individuals feel respected, are treated fairly, with an equitable opportunity to excel. To reinforce our mission, we launched a new global Diversity, Equity, and Inclusion (DEI) initiative in 2020. A key component of this initiative is our newly-formed Inclusion Advisory Council made up of employees from several different brands across the United States and Canada. Our council is currently focused on evaluating company policies, increasing employee awareness, and conducting employee listening sessions. Our goal is to create organizational change focusing on inclusion for all employees.

Health and Safety

We are committed to the health and safety of our employees and trade customers. During fiscal 2020, as a result of the COVID-19 pandemic, Rollins quickly implemented our pre-established business continuity plans. When state and local shelter-in-place restrictions were put in place, we experienced a smooth transition to a work-from-home environment for administrative staff and we limited traffic in and out of our branch locations. Employees receive regular emails with updated CDC guidelines, contact information for our Employee Assistance Program, and good news stories from various departments or branches to boost morale.

Community Involvement

We offer employees the opportunity to participate in various community outreach programs and believe that this commitment helps the Company to meet its goals of attracting, developing and retaining high-quality employees. We created Rollins United in 2019 to unify our brands’ philanthropic visions and consolidate our community outreach efforts. Our overarching goal is to create a significant impact in local communities over an extended period of time. The core mission of Rollins United is that everyone deserves a safe place to live, work, and play.

| 6 |

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to these reports, are available free of charge on our website at www.rollins.com, under the heading “Investor Relations – Filings and Reports – SEC Filings,” as soon as reasonably practicable after those reports are electronically filed with or furnished to the Securities and Exchange Commission (“SEC”).

| Item 1.A. | Risk Factors |

You should consider carefully the following risk factors before making an investment decision with respect to our securities. You are cautioned that the risk factors discussed below are not exhaustive.

Risks Related to our Brand and Certain Intellectual Property Rights

Our business depends on our strong brands and failing to maintain and enhance our brands and develop a positive client reputation could hurt our ability to retain and expand our base of customers.

Our strong brands, Rollins, Orkin, HomeTeam, Clark Pest Control, Western, Northwest, IFC, Crane Pest Control, Waltham, Trutech, PermaTreat, Critter Control, Safeguard Pest Control, Aardwolf Pestkare, OPC, and other strong brands have significantly contributed to the success of our business. Maintaining and enhancing our brands increases our ability to enter new markets and launch new and innovative services that better serve the needs of our customers. Our brands may be negatively impacted by a number of factors, including, among others, reputational issues and product/technical failures. Further, if our brands are significantly damaged, our business, operating results, and financial condition may be materially and adversely affected. We continue to develop strategies and innovative tools to gain a deeper understanding of customer acquisition, retention and client replacement in order to more effectively expand and retain our customer base. Maintaining and enhancing our brands will depend largely on our ability to remain a service leader and continue to provide high-quality pest control services that are truly beneficial and play a meaningful role in people’s lives.

Our brand recognition could be impacted if we are not able to adequately protect our intellectual property and other proprietary rights that are material to our business.

Our ability to compete effectively depends in part on our rights to service marks, trademarks, trade names and other intellectual property rights we own or license, particularly our registered brand names and service marks, Orkin®, Orkin Canada®, HomeTeam Pest Defense®, TAEXX®, Clark Pest Control®, Western Pest Services®, Northwest Exterminating®, Critter Control®, IFC®, Trutech®, Waltham Pest Services®, OPC Services®, Perma Treat Pest and Termite Control®, Crane Pest Control®, Murray Pest Control®, Allpest®, Statewide Pest Control®, Safeguard the Pest Control People®, Aardwolf Pestkare®, Adams Pest Control™, McCall® and others. Although we have sought to register or protect many of our marks either in the United States or in the countries in which they are or may be used, we have not sought to protect our marks in every country. Furthermore, because of the differences in foreign trademark, patent and other intellectual property or proprietary rights laws, we may not receive the same protection in other countries as we would in the United States. If we are unable to protect our proprietary information and brand names, we could suffer a material adverse impact on our reputation, business, financial position, results of operations and cash flows. Litigation may be necessary to enforce our intellectual property rights and protect our proprietary information, or to defend against claims by third parties that our products, services or activities infringe their intellectual property rights.

| 7 |

Our franchisees, subcontractors, and vendors could take actions that could harm our business.

Our franchisees, subcontractors, and vendors are contractually obligated to operate their businesses in accordance with the standards set forth in our agreements with them and applicable laws and regulations. Each franchised brand also provides training and support to franchisees. However, franchisees, subcontractors, and vendors are independent third parties that we do not control, and who own, operate and oversee the daily operations of their businesses. As a result, the ultimate success of any franchise operation rests with the franchisee. If franchisees do not successfully operate their businesses in a manner consistent with required standards, royalty payments to us will be adversely affected and our brands’ image and reputation could be harmed. This could materially adversely impact our business, financial position, results of operations and cash flows. Similarly, if subcontractors, vendors and franchisees do not successfully operate their businesses in a manner consistent with required laws, standards and regulations, we could be subject to claims from regulators or legal claims for the actions or omissions of such third-party distributors, subcontractors, vendors and franchisees. In addition, our relationship with our franchisees, subcontractors, and vendors could become strained (including resulting in litigation) as we impose new standards or assert more rigorous enforcement practices of the existing required standards. These strains in our relationships or claims could have a material adverse impact on our reputation, business, financial position, results of operations and cash flows.

From time to time, we receive communications from our franchisees regarding complaints, disputes or questions about our practices and standards in relation to our franchised operations and certain economic terms of our franchise arrangements. If franchisees or groups representing franchisees were to bring legal proceedings against us, we would vigorously defend against the claims in any such proceeding. Our reputation, business, financial position, results of operations and cash flows could be materially adversely impacted, and the price of our common stock could decline.

Risks Related to the Global Economy and Public Health Crises

Economic conditions may materially adversely affect our business.

Pest and termite services represent discretionary expenditures to many of our residential customers. If consumers restrict their discretionary expenditures, we may suffer a decline in revenues from our residential service lines. Economic downturns can also adversely affect our commercial customers, including food service, hospitality and food processing industries whose business levels are particularly sensitive to adverse economies. For example, we may lose commercial customers and related revenues because of consolidation or cessation of commercial businesses or because these businesses switch to a lower cost provider.

Our business, results of operations and financial condition is impacted by the coronavirus (COVID-19) pandemic and the restrictions put in place in connection therewith.

We have and continue to respond to the global outbreak of COVID-19 by taking steps to mitigate the potential risks posed to us by its spread and the impact of the restrictions put in place by the local, state and federal governments to protect the population. However, the resurgence of the COVID-19 pandemic in key areas of our operations may require us to implement additional restrictions on our operations. We continue to execute our business continuity plan and have implemented a comprehensive set of new protocols for the health and safety of our employees, customers, and business partners, such as wearing masks, gloves, and other personal protective equipment, social distancing, utilizing electronic documents and sanitizing high touch surfaces, among others. Our employees transitioned to work-from-home during fiscal 2020 where appropriate. However, due to the speed and scope with which the COVID-19 situation has evolved and the uncertainty of its duration and the timing of recovery, we are not able at this time to predict the extent to which the COVID-19 pandemic may have a material effect on our results of operations or financial condition. In addition, the unprecedented uncertainty surrounding COVID-19, due to rapidly changing governmental directives, public health challenges and progress, macroeconomic consequences, and market reactions thereto, also makes it more challenging for our management to estimate the future performance of our business and develop strategies to generate growth or achieve our objectives for 2021 and beyond.

Risks Related to our Labor Force

Our inability to attract and retain skilled workers may impair growth potential and profitability.

Our ability to remain productive and profitable will depend substantially on our ability to attract and retain sales and service operations professional workers, develop leadership and implement diversity, equity and inclusion initiatives. Our ability to expand our operations is in part impacted by our ability to increase our labor force. The demand for employees is high, and the supply is limited. A significant increase in the wages paid and benefits offered by competing employers could result in a reduction in our labor force, increases in our labor costs, or both. If either of paid these events occurred, our capacity and profitability could be diminished, and our growth potential could be impaired.

| 8 |

Risks Related to our Business, Industry and Operations

We face risks regarding our ability to maintain our competitive position in the pest control industry in the future.

We operate in a highly competitive industry. Our revenues and earnings are affected by changes in competitors’ prices and general economic issues. We compete with other large pest control companies, as well as numerous smaller pest control companies, for a finite number of customers. We believe that the principal competitive factors in the market areas that we serve are service quality, terms of guarantees, reputation for safety, technical proficiency and price. Although we believe that our experience and reputation for safety and quality service are excellent, we cannot assure investors that we will be able to maintain our competitive position.

We may not be able to identify, complete or successfully integrate acquisitions.

Acquisitions have been and may continue to be an important element of our business strategy. We cannot assure investors that we will be able to identify and acquire acceptable acquisition candidates on terms favorable to us in the future. We cannot assure investors that we will be able to integrate successfully the operations and assets of any acquired business with our own business. Any inability on our part to integrate and manage the growth from acquired businesses could have a material adverse effect on our results of operations and financial condition.

Expanding into international markets presents unique challenges, and our expansion efforts with respect to international operations may not be successful.

An element of our strategy includes further expansion into international markets. Our ability to successfully operate in international markets may be adversely affected by political, economic and social conditions beyond our control, local laws and customs, and legal and regulatory constraints, including compliance with applicable anti-corruption and currency laws and regulations, of the countries or regions in which we currently operate or intend to operate in the future. Risks inherent in our existing and future international operations also include, among others, the costs and difficulties of managing international operations, difficulties in identifying and gaining access to local suppliers, suffering possible adverse tax consequences from changes in tax laws or the unfavorable resolution of tax assessments or audits, maintaining product quality and greater difficulty in enforcing intellectual property rights. Additionally, foreign currency exchange rates and fluctuations may have an adverse effect on the financial results of our international operations.

Our operations are affected by adverse weather conditions.

Our operations are directly impacted by the weather conditions worldwide. The business of the Company is affected by the seasonal nature of the Company’s pest and termite control services. The increase in pest presence and activity, as well as the metamorphosis of termites in the spring and summer (the occurrence of which is determined by the timing of the change in seasons), has historically resulted in an increase in the revenue and income of the Company’s pest and termite control operations during such periods. The business of the Company is also affected by extreme weather such as drought which can greatly reduce the pest population for extended periods.

| 9 |

Risks Related to Cybersecurity, Privacy Compliance and Business Disruptions

The Company and its wholly-owned subsidiaries could suffer disruption to business operations and face economic and reputational damage, as well as be subject to fines, penalties and private litigation, if there is unauthorized access to or unintentional distribution of personal, financial, proprietary, confidential, or other protected data or information the Company is entrusted to keep about its customers, employees, business practices, or third parties.

Our internal information technology (“IT”) systems contain certain personal, financial, health, or other protected and confidential information that is entrusted to us by our customers and employees. Our IT systems also contain the Company’s and its wholly-owned subsidiaries’ proprietary and other confidential information related to our business, such as business plans, customer lists and product and service development initiatives. We also grant third-party business partners and service providers access to such information in order to facilitate business operations and administer benefits. Employees, third-party business partners, and service providers can knowingly or unknowingly disseminate such information or serve as an entry point for bad actors to access such information. Vulnerabilities from growth, acquisitions, and integration with new systems also exist.

Our privacy compliance and digital risk management initiatives focus on the threats and risks to enterprise information and the underlying IT systems processing such information as part of the implementation of business processes. The Company also relies on, among other things, commercially available vendors, cyber protection systems, software, tools and monitoring to provide security for processing, transmission and storage of protected information and data. The systems currently used for transmission and approval of payment card transactions, and the technology utilized in payment cards themselves, all of which can put payment card data at risk, meet standards set by the payment card industry (“PCI”). We have also implemented policies and procedures, internal training, system controls, and constant monitoring and audit processes to protect the Company from internal and external vulnerabilities and to comply with consumer privacy laws in the areas in which we operate. Further, the Company limits retention of certain data, encrypts certain data and otherwise protects information to comply with consumer privacy laws in the areas in which we operate.

We continue to evaluate and modify our systems and protocols for data security compliance purposes, and such standards may change from time to time. We monitor certain third-party business partners and service providers for compliance and vulnerabilities. Activities by bad actors, changes in computer and software capabilities and encryption technology, new tools and discoveries, cloud applications, changes in multi-jurisdictional regulations, and other events or developments may result in a compromise or breach of our systems. Any compromises, breaches, application errors or human mistakes related to our systems or failures to comply with applicable standards could not only disrupt our financial operations, including our customers’ ability to pay for our services and products by credit card or their willingness to purchase our services and products, but could also result in violations of applicable laws, regulations, orders, industry standards or agreements and subject us to costs, penalties and liabilities which could have a material adverse impact on our reputation, business, financial position, results of operations and cash flows. Furthermore, a breach of data security or failure to comply with rigorous multi-jurisdictional consumer privacy requirements could expose us to customer litigation, regulatory actions and costs related to the reporting and handling of such a violation or breach.

Risks Related to Legal, Regulatory and Risk Management Matters

We are from time to time subject to lawsuits, investigations and other proceedings which could have a material adverse effect on our business, financial condition and results of operations, and our operations may be adversely affected if we fail to comply with applicable law or other governmental regulations, including environmental and other regulations relating to the pest control industry.

| 10 |

In the normal course of business, we are involved in various claims, arbitrations, contractual disputes, investigations and litigation, including claims that our services or vehicles caused damage or injury, claims that our services did not achieve the desired results, claims related to acquisitions, allegations by federal, state or local authorities, including the SEC, of violations of regulations or statutes, claims related to wage and hour law violations and claims related to environmental matters. These claims, proceedings or litigation, either alone or in the aggregate, could have a material adverse effect on our business, financial condition and results of operations.

Additionally, our business is significantly affected by and subject to regulation by various federal, state, provincial, regional and local governments in the countries in which we operate, including, but not limited to, environmental laws, antitrust laws, consumer protection laws, employment laws, including wage and hour laws, payroll taxes and anti-discrimination laws, immigration, human health and safety laws and other regulations relating to the pest control industry.

We are unable to predict whether such laws will, in the future, materially affect our operations and financial condition or whether any changes will require us to incur substantial increases in costs in order to comply with such changes. Penalties for noncompliance with these laws may include investigations, criminal sanctions or civil remedies, including, but not limited to, cancellation of licenses, fines, and other corrective actions, which could negatively affect our business, financial condition and results of operations.

The ongoing SEC investigation and any potential related litigation entail risks and uncertainties.

The SEC is conducting an investigation, which the Company believes is primarily focused on how it established accruals and reserves at period-ends and the impact of those accruals and reserves on reported earnings. The investigation relates to period-ends for periods beginning January 1, 2015. The Company is fully cooperating with the SEC’s investigation. The Company’s Audit Committee retained independent counsel to conduct an internal investigation into matters related to the SEC investigation and, in particular, the Company’s processes for establishing and adjusting reserves for each quarter in the relevant periods. The internal investigation was concluded in October 2020. Based on the results of the internal investigation, it was determined that there was a significant deficiency in the Company’s internal controls relating to the documentation and review of accounting entries for certain reserves and accruals. The Company has subsequently reevaluated and strengthened its internal controls over financial reporting, including improving processes and procedures and supporting documentation and providing additional training, which has resulted in the remediation of the significant deficiency. The Company, after consultation with the Audit Committee and independent counsel, believes that its financial statements filed with the SEC on Forms 10-K and 10-Q for the relevant periods fairly present in all material respects its financial condition, results of operations and cash flows as of their respective balance sheet dates and for the periods then ended.

The SEC’s investigation is ongoing, however, and there can be no assurance that the SEC or another regulatory body will not make further regulatory inquiries or pursue action against the Company and its senior officers that could result in potentially significant sanctions and penalties, or that could require the Company to take additional remedial steps. Potential sanctions against the Company and/or individuals could include penalties, injunctions, and cease-and-desist orders. Further, the Company may be subject to litigation from third parties related to the matters under review by the SEC. Accordingly, the ongoing SEC investigation and any potential related litigation could result in distraction to management and entail risks and uncertainties the outcome of which could adversely affect our financial results and our reputation.

Product, service or other related liability claims could have a material adverse effect on our liquidity, financial position and results of operations.

The handling, storage, transportation, and use of chemical products required to provide pest control service involves inherent exposure to potential product liability claims, service level claims, and related adverse publicity. Additionally, hazards could potentially cause injury, damage to, or destruction of, property or equipment and environmental contamination or other environmental damage, which could have an adverse effect on our business, financial condition or results of operations. Also, the occurrence of disruptions, shutdowns or other material operating problems at our facilities or those of our suppliers or customers due to any of these risks could adversely affect our reputation and have a material adverse effect on our operations as a whole, including our results of operations and cash flows, both during and after the period of operational difficulties. We maintain product and general liability insurance, however, there can be no assurance that the types or levels of coverage maintained are adequate to cover these potential significant and catastrophic risks. In addition, we may not be able to continue to maintain our existing insurance coverage or obtain comparable or additional insurance coverage at a reasonable cost, if at all, in the event a significant product or service claim arises.

| 11 |

Our risk management and safety programs may not have the intended effect of reducing our liability for personal injury or property loss.

Our safety record is critical to our reputation. Many of our clients require that we meet certain safety criteria to be eligible to provide service and bid for contracts, and many contracts provide for automatic termination or forfeiture of some or all of our contract fees or profit in the event we fail to meet certain measures. Accordingly, if we fail to maintain adequate safety standards, we could suffer reduced profitability or the loss of projects or clients, which could have a material adverse impact on our business, financial condition and results of operations.

We attempt to mitigate risks relating to personal injury or property loss through the implementation of company-wide safety management efforts designed to decrease the incidence of accidents or events that may occur. It is expected that any such decreases could also have the effect of reducing our insurance costs. However, incidents involving injury or property loss may be caused by multiple potential factors, a significant number of which are beyond our control. Therefore, there is no guarantee that our risk management and safety programs will have the desired effect of controlling all potential costs and liability exposure.

Our enterprise risk management program may leave us exposed to unidentified or unanticipated risks.

We maintain an enterprise risk management program that is designed to identify, assess, mitigate, and monitor the risks that we face. There can be no assurance that our frameworks or models for assessing and managing known risks, compliance with applicable law, and related controls will effectively mitigate risk and limit losses in all market environments or against all types of known and unknown risk in our business. If conditions or circumstances arise that expose flaws or gaps in our risk management or compliance programs, the performance and value of our business could be materially adversely affected.

The Company maintains insurance and other traditional risk-shifting tools to manage certain types of risks. However, such tools are subject to terms such as deductibles, retentions, limits and policy exclusions, as well as risk of denial of coverage, default or insolvency. If we suffer unexpected or uncovered losses, or if any of our insurance policies are terminated for any reason or are not effective in mitigating our risks, we may incur losses that are not covered or that exceed our coverage limits and could adversely impact our results of operations, cash flows and financial position.

Risks Related to our Capital and Ownership Structure

The Company’s management has a substantial ownership interest; public stockholders may have no effective voice in the Company’s management.

The Company has elected the “Controlled Company” exemption under Section 303A of the New York Stock Exchange (“NYSE”) Listed Company Manual. The Company is a “Controlled Company” because a group that includes the Company’s Chairman of the Board and Chief Executive Officer, Gary W. Rollins, and certain companies under his control, controls in excess of fifty percent of the Company’s voting power. As a “Controlled Company,” the Company need not comply with certain NYSE rules.

Rollins, Inc.’s executive officers, directors and their affiliates hold directly, or through indirect beneficial ownership, in the aggregate, approximately 54 percent of the Company’s outstanding shares of common stock. As a result, these persons will effectively control the operations of the Company, including the election of directors and approval of significant corporate transactions such as acquisitions and approval of matters requiring stockholder approval. This concentration of ownership could also have the effect of delaying or preventing a third party from acquiring control of the Company at a premium.

| 12 |

Our management has a substantial ownership interest, and the availability of the Company’s common stock to the investing public may be limited.

The availability of Rollins’ common stock to the investing public would be limited to those shares not held by the executive officers, directors and their affiliates, which could negatively impact Rollins’ stock trading prices and affect the ability of minority stockholders to sell their shares. Future sales by executive officers, directors and their affiliates of all or a portion of their shares could also negatively affect the trading price of our common stock.

Provisions in Rollins, Inc.’s certificate of incorporation and bylaws may inhibit a takeover of the Company.

Rollins, Inc.’s certificate of incorporation, bylaws and other documents contain provisions including advance notice requirements for stockholder proposals and staggered terms for the Board of Directors. These provisions may make a tender offer, change in control or takeover attempt that is opposed by the Company’s Board of Directors more difficult or expensive.

| Item 1.B. | Unresolved Staff Comments |

None.

| Item 2. | Properties. |

The Company’s administrative headquarters are owned by the Company, and are located at 2170 Piedmont Road, N.E., Atlanta, Georgia 30324. The Company owns or leases over 550 branch offices and operating facilities used in its business as well as the Rollins Training Center located in Atlanta, Georgia, the Rollins Customer Service Center located in Covington, Georgia, and the Pacific Division Administration and Training Center in Riverside, California. None of the branch offices, individually considered, represents a materially important physical property of the Company. The facilities are suitable and adequate to meet the current and reasonably anticipated future needs of the Company.

| Item 3. | Legal Proceedings. |

In the normal course of business, the Company and its subsidiaries are involved in, and will continue to be involved in, various claims, arbitrations, contractual disputes, investigations, and regulatory and litigation matters relating to, and arising out of, our businesses and our operations. These matters may involve, but are not limited to, allegations that our services or vehicles caused damage or injury, claims that our services did not achieve the desired results, claims related to acquisitions and allegations by federal, state or local authorities of violations of regulations or statutes. In addition, we are parties to employment-related cases and claims from time to time, which may include claims on a representative or class action basis alleging wage and hour law violations. We are also involved from time to time in certain environmental matters primarily arising in the normal course of business. We evaluate pending and threatened claims and establish loss contingency reserves based upon outcomes we currently believe to be probable and reasonably estimable. We do not believe that the ultimate resolution of the claims we are currently involved in will have a material adverse effect on our business, results of operations, financial condition, cash flow and prospects; however, it is possible that an unfavorable outcome of some or all of the matters, however unlikely, could result in a charge that might be material to the results of an individual quarter or year.

As previously disclosed, the SEC is conducting an investigation, which the Company believes is primarily focused on how it established accruals and reserves at period-ends and the impact of those accruals and reserves on reported earnings. The investigation relates to period-ends for periods beginning January 1, 2015. The Company is fully cooperating with the SEC’s investigation. The Company cannot predict the outcome of this investigation. The Company’s Audit Committee retained independent counsel to conduct an internal investigation into matters related to the SEC investigation and, in particular, the Company’s processes for establishing reserves for each quarter in the relevant periods. The internal investigation was concluded in October 2020. The Company, after consultation with the Audit Committee and the independent counsel, believes that its financial statements filed with the SEC on Forms 10-K and 10-Q for the relevant periods fairly present in all material respects its financial condition, results of operations and cash flows as of their respective balance sheet dates and for the periods then ended. See Part I, Item 1.A. for additional discussion of related Risk Factors.

See Note 15 to Part I, Item 1 for discussion of certain litigation.

| 13 |

Management does not believe that any pending claim, proceeding or litigation, either alone or in the aggregate, will have a material adverse effect on the Company’s financial position, results of operations or liquidity; however, it is possible that an unfavorable outcome of some or all of the matters, however unlikely, could result in a charge that might be material to the results of an individual quarter or year.

| Item 4. | Mine Safety Disclosures. |

Not applicable.

| Item 4.A. | Information about our Executive Officers. |

Each of the executive officers of the Company was elected by the Board of Directors to serve until the Board of Directors’ meeting immediately following the next Annual Meeting of Stockholders or until his or her earlier removal by the Board of Directors or his or her resignation. The following table lists the executive officers of the Company and their ages, offices within the Company, and the dates from which they have continually served in their present offices with the Company.

| Name | Age | Office with Registrant | Date First Elected to Present Office | |||||

| Gary W. Rollins (1) | 76 | Chairman and Chief Executive Officer | August 25, 2020 | |||||

| John F. Wilson (2) | 63 | Vice Chairman and Assistant to the Chairman | August 25, 2020 | |||||

| Jerry E. Gahlhoff Jr. (3) | 48 | President and Chief Operating Officer | August 25, 2020 | |||||

| Paul E. Northen (4) | 56 | Senior Vice President, Chief Financial Officer and Treasurer | January 26, 2016 | |||||

| Elizabeth B. Chandler (5) | 57 | Vice President, General Counsel and Corporate Secretary | January 1, 2018 | |||||

| (1) | Gary W. Rollins was named Chairman of Rollins, Inc in August 2020. He was elevated to Vice Chairman of Rollins, Inc. in January 2013. He was elected to the office of Chief Executive Officer in July 2001. In February 2004, he was named Chairman of Orkin, LLC. |

| (2) | John Wilson joined the Company in 1996 and has held various positions of increasing responsibility, serving as a technician, sales inspector, branch manager, region manager, vice president and division president. His most senior positions have included President and Chief Operating Officer of Rollins, Inc., Vice President of Rollins, Inc., Southeast Division President, Atlantic Division Vice President and Central Commercial Region Manager. Mr. Wilson was elevated to Vice Chairman in August 2020. |

| (3) | Jerry E. Gahlhoff Jr. was named the President and Chief Operating Officer of Rollins, Inc. in August 2020. He came to the Company in the HomeTeam acquisition in 2008 and has successfully managed several areas of the Company with increasing responsibility. He most recently led the Rollins Specialty Brands team of HomeTeam, Clark, Northwest, Western Pest, Waltham Pest, OPC pest control companies as well as the Rollins Human Resources department. |

| (4) | Paul E. Northen joined Rollins in 2015 as Chief Financial Officer and Treasurer. He was promoted to Vice President of Rollins, Inc. in January 2016, and Senior Vice President of Rollins, Inc. in April 2018. He began his career with UPS in 1985 and brings a wealth of tax, risk management and audit experience as well as strong international exposure to Rollins. Prior to joining Rollins, Mr. Northen was Vice President of International Finance and Accounting-Global Business Services for UPS. He previously held the positions of Chief Financial Officer of UPS’ Asia Pacific Region based in Hong Kong, and as Vice President of Finance in UPS’ Pacific and Western Regions. |

| (5) | Elizabeth (Beth) Brannen Chandler joined Rollins in 2013 as Vice President and General Counsel. In 2017, Beth assumed responsibility for the Risk Management and Internal Audit groups. She was appointed to Corporate Secretary in January 2018. Before joining Rollins, Ms. Chandler was Vice President, General Counsel and Corporate Secretary for Asbury Automotive. Prior to working with Asbury, Ms. Chandler served as city attorney for the City of Atlanta; and she served as Vice President, Assistant General Counsel and Corporate Secretary for Mirant Corp. |

| 14 |

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

The common stock of the Company is listed on the New York Stock Exchange and is traded on the Philadelphia, Chicago and Boston Exchanges under the symbol ROL.

As of January 31, 2021, there were 7,760 holders of record of the Company’s common stock. However, a large number of our shareholders hold their shares in “street name” in brokerage accounts and, therefore, do not appear on the shareholder list maintained by our transfer agent.

Issuer Purchases of Equity Securities

During the years ended December 31, 2020 and 2019, the Company did not repurchase shares on the open market. In total, there remains 11.4 million additional shares authorized to be repurchased under prior Board approval. The repurchase program does not have an expiration date.

| Period | Total number of shares purchased (1) | Weighted average price paid per share | Total number of shares purchased as part of publicly announced repurchase plans (2) | Maximum number of shares that may yet be purchased under the repurchase plans | ||||||||||||

| October 1 to 31, 2020 | 703 | $ | 35.87 | — | 11,415,625 | |||||||||||

| November 1 to 30, 2020 | 2,147 | 39.67 | — | 11,415,625 | ||||||||||||

| December 1 to 31, 2020 | — | — | — | 11,415,625 | ||||||||||||

| Total | 2,850 | $ | 38.73 | — | 11,415,625 | |||||||||||

| (1) | Includes repurchases from employees for the payment of taxes on vesting of restricted shares in the following amounts: October 2020: 703; November 2020: 2,147; and December 2020: 0. |

| (2) | In 2012, the Company’s Board authorized a share repurchase plan to repurchase up to 5.0 million shares of the Company’s common stock. The split-adjusted authorized shares under the share repurchase plan are 16.9 million shares. |

| 15 |

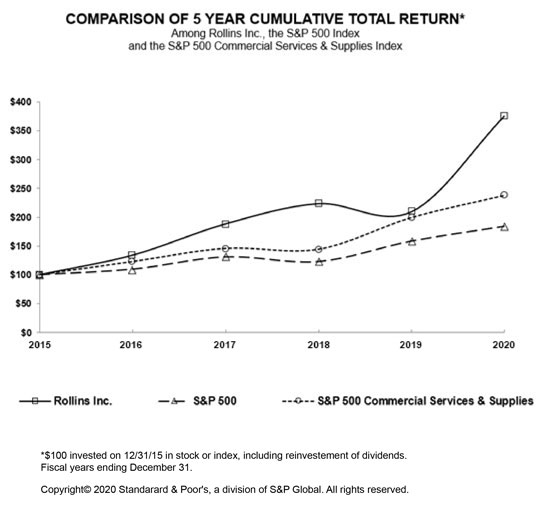

PERFORMANCE GRAPH

The following graph sets forth a five-year comparison of the cumulative total stockholder return based on the performance of the stock of the Company as compared with both a broad equity market index and an industry index. The indices included in the following graph are the S&P 500 Index and the S&P 500 Commercial Services Index.

COMPARISON OF FIVE YEAR CUMULATIVE TOTAL RETURN*

Copyright© 2020 Standard & Poor’s, a division of S&P Global. All rights reserved.

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |||||||||||||||||||

| Rollins Inc. | 100.00 | 133.86 | 188.22 | 223.35 | 209.10 | 375.31 | ||||||||||||||||||

| S&P500 | 100.00 | 109.54 | 130.81 | 122.65 | 158.07 | 183.77 | ||||||||||||||||||

| S&P 500 Commercial Services & Supplies | 100.00 | 122.83 | 145.76 | 144.16 | 199.28 | 237.88 | ||||||||||||||||||

ASSUMES INITIAL INVESTMENT OF $100

*TOTAL RETURN ASSUMES REINVESTMENT OF DIVIDENDS

NOTE: TOTAL RETURNS BASED ON MARKET CAPITALIZATION

| 16 |

| Item 6. | Selected Financial Data |

The following summary financial data of Rollins highlights selected financial data and should be read in conjunction with the audited financial statements and related notes included elsewhere in this document.

All share and per share data presented in the following table have been adjusted for the three-for-two stock split effective December 10, 2020.

FIVE-YEAR FINANCIAL SUMMARY

| STATEMENT OF OPERATIONS DATA | ||||||||||||||||||||

| (in thousands except per share data) | ||||||||||||||||||||

| Years ended December 31, | 2020 | 2019 | 2018 | 2017 | 2016 | |||||||||||||||

| Revenues | $ | 2,161,220 | $ | 2,015,477 | $ | 1,821,565 | $ | 1,673,957 | $ | 1,573,477 | ||||||||||

| Income before taxes | $ | 354,720 | $ | 261,160 | $ | 310,733 | $ | 294,502 | $ | 260,636 | ||||||||||

| Net income | $ | 260,824 | $ | 203,347 | $ | 231,663 | $ | 179,124 | $ | 167,369 | ||||||||||

| Earnings per share - Basic | $ | 0.53 | $ | 0.41 | $ | 0.47 | $ | 0.37 | $ | 0.34 | ||||||||||

| Earnings per share - Diluted | $ | 0.53 | $ | 0.41 | $ | 0.47 | $ | 0.37 | $ | 0.34 | ||||||||||

| Dividends per share | $ | 0.33 | $ | 0.31 | $ | 0.31 | $ | 0.25 | $ | 0.22 | ||||||||||

| OTHER DATA: | ||||||||||||||||||||

| Net cash provided by operating activities | $ | 435,785 | $ | 319,573 | $ | 299,401 | $ | 235,370 | $ | 226,525 | ||||||||||

| Net cash used in investing activities | $ | (162,395 | ) | $ | (455,107 | ) | $ | (101,375 | ) | $ | (154,175 | ) | $ | (76,842 | ) | |||||

| Net cash (used in)/provided by financing activities | $ | (281,273 | ) | $ | 111,686 | $ | (175,412 | ) | $ | (130,263 | ) | $ | (136,371 | ) | ||||||

| Depreciation | $ | 40,623 | $ | 36,646 | $ | 30,364 | $ | 27,381 | $ | 24,725 | ||||||||||

| Amortization of intangible assets | $ | 47,706 | $ | 44,465 | $ | 36,428 | $ | 29,199 | $ | 26,177 | ||||||||||

| Capital expenditures | $ | (23,229 | ) | $ | (27,146 | ) | $ | (27,179 | ) | $ | (24,680 | ) | $ | (33,081 | ) | |||||

| BALANCE SHEET DATA AT END OF YEAR: | ||||||||||||||||||||

| Current assets | $ | 314,777 | $ | 309,787 | $ | 286,021 | $ | 262,795 | $ | 290,171 | ||||||||||

| Total assets | $ | 1,845,900 | $ | 1,744,376 | $ | 1,094,124 | $ | 1,033,663 | $ | 916,538 | ||||||||||

| Total debt | $ | 203,000 | $ | 291,500 | $ | — | $ | — | $ | — | ||||||||||

| Stockholders’ equity | $ | 941,360 | $ | 815,750 | $ | 711,908 | $ | 653,924 | $ | 568,545 | ||||||||||

| Number of shares outstanding at year-end | 491,612 | 491,146 | 490,962 | 490,482 | 490,031 | |||||||||||||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Presentation

This discussion should be read in conjunction with our audited financial statements and related notes included elsewhere in this document. Discussions of 2018 items and year-to-year comparisons of 2019 and 2018 that are not included in this Form 10-K can be found in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 on our Annual report on Form 10-K for the year ended December 31, 2019. The following discussion (as well as other discussions in this document) contains forward-looking statements. Please see “Cautionary Statement Regarding Forward-Looking Statements” for a discussion of uncertainties, risks and assumptions associated with these statements.

The Company

Rollins, Inc. (the “Company”) is an international service company with headquarters located in Atlanta, Georgia, providing pest and termite control services through its wholly-owned subsidiaries to both residential and commercial customers in the United States, Canada, Australia, Europe, and Asia with international franchises in Canada, Central and South America, the Caribbean, the Middle East, Asia, Europe, Africa, and Australia. Services are performed through a contract that specifies the treatment and the pricing arrangement with the customer.

| 17 |

The Company has one reportable segment, its pest and termite control business. The Company’s results of operations and its financial condition are not reliant upon any single customer or a few customers or the Company’s foreign operations.

Overview

RESULTS OF OPERATIONS

| (in thousands) | % Better/(worse) compared to prior year | |||||||||||||||||||

| Years ended December 31, | 2020 | 2019 | 2018 | 2020 | 2019 | |||||||||||||||

| Revenues | $ | 2,161,220 | $ | 2,015,477 | $ | 1,821,565 | 7.2 | 10.6 | ||||||||||||

| Cost of services provided | 1,048,592 | 993,593 | 894,437 | (5.5 | ) | (11.1 | ) | |||||||||||||

| Depreciation and amortization | 88,329 | 81,111 | 66,792 | (8.9 | ) | (21.4 | ) | |||||||||||||

| Sales, general and administrative | 656,207 | 623,379 | 550,698 | (5.3 | ) | (13.2 | ) | |||||||||||||

| Accelerated stock vesting expense | 6,691 | — | — | |||||||||||||||||

| Pension settlement loss | — | 49,898 | — | N/M | N/M | |||||||||||||||

| Loss/(gain) on sales of assets, net | 1,599 | (581 | ) | (875 | ) | (375.2 | ) | (33.6 | ) | |||||||||||

| Interest expense/(income), net | 5,082 | 6,917 | (220 | ) | 26.5 | N/M | ||||||||||||||

| Income before income taxes | 354,720 | 261,160 | 310,733 | 35.8 | (16.0 | ) | ||||||||||||||

| Provision for income taxes | 93,896 | 57,813 | 79,070 | (62.4 | ) | 26.9 | ||||||||||||||

| Net income | $ | 260,824 | $ | 203,347 | $ | 231,663 | 28.3 | (12.2 | ) | |||||||||||

General Operating Comments

2020 marked the Company’s 23rd consecutive year of increased revenues. Revenues for the year rose 7.2 percent to $2.161 billion compared to $2.015 billion for the prior year. Income before income taxes increased 35.8% to $354.7 million compared to $261.2 million the prior year. Net income increased 28.3% to $260.8 million, with earnings per diluted share of $0.53 compared to $203.3 million, or $0.41 per diluted share for the prior year. The drop in net income from 2018 to 2019 was primarily attributed to the pension settlement loss recorded in 2019.

COVID-19 Pandemic Impact

As the pandemic challenges grew early in 2020, the Company made numerous operational adjustments to address the economic, health and safety challenges from the COVID-19 pandemic. These included new COVID-related procedures, modified customer service and related protocols, daily health screenings before entering shared offices, and a transition to remote work locations to reduce concentrations of personnel in offices where appropriate. Cost containment efforts included furloughs, layoffs, elimination of non-essential travel, postponing capital expenditures, and temporary salary reductions for upper management, among other actions.

Customer retention during the pandemic is less predictable, and of greater immediate concern compared with our normal operations, however, our residential pest and termite control business has remained reasonably consistent with some growth over prior years. With many sheltering or working from home, we have experienced higher than normal demand for our residential services. Our commercial pest control business has been more adversely impacted, as it crosses multiple industries such as healthcare, food processing, logistics, grocery, retail and hospitality. Each of these industries is being impacted differently by the pandemic. Many of our commercial customers continue to operate as “essential” businesses; however, unfortunately there are a notable number of others that have closed, at least temporarily. We expect this impact will persist through much of 2021 until the majority of the population has been vaccinated against the virus. The Company’s residential and termite revenues grew 13.4% and 9.6%, respectively, in 2020 compared to 2019 while our commercial pest control revenues fell by 0.5%.

| 18 |

While we have a substantial amount of intangible assets on our balance sheet, based on our revenue growth this year, we do not anticipate any significant long-term loss in revenues or cash flows that would approach a level for impairment of intangible assets.

All of our critical supply-chain vendors have remained operational, and we have engaged additional new sources to supplement our existing suppliers, especially for critical PPE and other COVID-19 related items. Fleet suppliers and support vendors continue to serve our needs.

Results of Operations—2020 Versus 2019

Overview

The Company’s revenues increased to $2.161 billion in 2020, a 7.2% increase compared to 2019. Gross margin increased to 51.5% for 2020 from 50.7% in 2019. Sales, general and administrative expense were 30.4% of revenues in 2020 compared to 30.9% in 2019. The Company’s depreciation and amortization expense as a percent of revenue increased 2.5% to 4.1% in 2020 compared to 4.0% in 2019. Rollins’ net income of $260.8 million in 2020 was an increase of $57.5 million, or 28.3%, compared to $203.3 million in 2019. Net profit margin improved to 12.1% in 2020 from 10.1% in 2019. Rollins continued to expand our global brand recognition with acquisitions in the United States, Canada, United Kingdom, Australia, and Asia as well as expanded our Orkin international franchise program in numerous countries around the globe. The Company continues to seek new international opportunities.

Revenues

Revenues for the year ended December 31, 2020 were $2.161 billion, an increase of $145.7 million, or 7.2%, from 2019 revenues of $2.015 billion. Growth accounted for approximately 3.8% of our increase, and our acquisitions contributed the remaining revenue growth. We experienced strong growth in residential pest control, increasing 13.4%, while termite and ancillary revenues grew 9.6%. Year over year commercial revenues were down 0.5% as commercial pest control was negatively impacted by the COVID-19 virus due to various levels of government-driven shutdowns. The Company’s revenue mix for the year ended December 31, 2020 consisted primarily of 45% residential pest control, 36% commercial pest control and 19% termite and ancillary revenues (such as moisture control, insulation, deck and gutter work).

During 2020, the Company chose to forgo the normal mid-year price increase, which historically contributes approximately 1.0% to our annual revenue growth. Approximately 80% of the Company’s pest control revenue was recurring in 2020, as well as in 2019.

The Company’s foreign operations accounted for approximately 7% and 8% of total revenues for the years ended December 31, 2020 and 2019, respectively. The Company established new franchises in several international countries around the globe in 2020 while closing or acquiring others, for a total of 94 Orkin international franchises and nine Australia franchises at December 31, 2020, compared to 97 Orkin international franchises, one Canadian Critter Control franchises and ten Australia franchises at December 31, 2019. The Australia franchises operate under the Murray Pest Control and Scientific Pest Management names.

Revenue from franchising was up 5.6% in 2020 compared to 2019 as the Company continued to expand Orkin’s international footprint and recognition of initial franchise fees. International and domestic franchising revenue was less than 1% of the Company’s revenues for 2020. Orkin had 143 and 147 franchises (domestic and international) at December 31, 2020 and 2019, respectively. The Company continued its strategy of buying back Critter Control franchises during 2020, resulting in a drop in franchises to 79 at December 31, 2020, compared to 85 at December 31, 2019.

Cost of Services Provided

For the twelve months ended December 31, 2020, cost of services provided increased $55.0 million, or 5.5%, compared to the twelve months ended December 31, 2019. Gross margin for the year increased to 51.5% for 2020 from 50.7% in 2019. Margin improvements were driven primarily from lower service wage growth compared to revenue growth, and from fleet savings driven by improvements in our routing and scheduling efficiencies and lower fuel prices.

| 19 |

Depreciation and Amortization

For the twelve months ended December 31, 2020, depreciation and amortization increased $7.2 million, or 8.9%, compared to the twelve months ended December 31, 2019. The dollar increase was primarily due to depreciation increasing $4.0 million, or 10.9%, from the depreciation of acquired and purchased assets and depreciation from various IT related projects. Amortization of intangible assets increased $3.2 million, or 7.3%, for 2020 due to the additional amortization of customer contracts from several acquisitions over the last year, including a full year of amortization for Clark Pest Control acquired in April 2019, as well as several smaller foreign and domestic companies.

Sales, General and Administrative

For the twelve months ended December 31, 2020, sales, general and administrative (SG&A) expenses increased $32.8 million, or 5.3%, compared to the twelve months ended December 31, 2019. SG&A decreased to 30.4% of revenues for the year ended December 31, 2020 compared to 30.9% in 2019. The Company eliminated any non-essential spending at the start of the pandemic which lowered expenses in several areas. Travel restrictions reduced typical training, site visits and conference costs. Conversely, we incurred higher than normal expenses in 2019 related to acquisition preparation and integration activities for Clark Pest Control.

Gain / Loss on Sales of Assets, Net

The Company recorded a $1.6 million net loss on sales of assets for the year ended December 31, 2020 compared to a net gain on sales of assets of $0.6 million in 2019. The Company’s 2020 losses came primarily from liquidating the pension plan assets from the 2019 pension plan settlement. During 2019, the Company recorded gains from the sale of owned vehicles and other owned property.

Interest Expense, Net

Interest expense, net for the years ended December 31, 2020 and 2019 was $5.1 million and $6.9 million respectively, driven largely by borrowings to fund acquisitions, among other things.

Taxes

The Company’s effective tax rate increased to 26.5% in 2020 compared to 22.1% in 2019, due primarily to state and foreign income tax changes and limited tax deductibility for the accelerated stock vesting expense recognized in 2020. The 2019 rate was lower due to beneficial adjustments related to the 2019 pension settlement.

Liquidity and Capital Resources

Cash and Cash Flow

Cash from operating activities is the principal source of cash generation for our businesses.

The most significant source of cash in Rollins’ cash flow from operations is customer-related activities, the largest of which is collecting cash resulting from services sold. The most significant operating use of cash is to pay our suppliers, employees, tax authorities and others for a wide range of material and services.

| 20 |

The Company’s cash and cash equivalents at December 31, 2020, 2019, and 2018 were $98.5 million, $94.3 million, and $115.5 million, respectively.

| (in thousands) | ||||||||||||

| Years ended December 31, | 2020 | 2019 | 2018 | |||||||||

| Net cash provided by operating activities | $ | 435,785 | $ | 319,573 | $ | 299,401 | ||||||

| Net cash used in investing activities | (162,395 | ) | (455,107 | ) | (101,375 | ) | ||||||

| Net cash (used in)/provided by financing activities | (281,273 | ) | 111,686 | (175,412 | ) | |||||||

| Effect of exchange rate on cash | 12,084 | 2,639 | (14,179 | ) | ||||||||

| Net increase/(decrease) in cash and cash equivalents | $ | 4,201 | $ | (21,209 | ) | $ | 8,435 | |||||

Cash Provided by Operating Activities

The Company’s operations generated cash of $435.8 million for the year ended December 31, 2020 primarily from net income of $260.8 million, compared with cash provided by operating activities of $319.6 million in 2019 and $299.4 million in 2018. The Company believes its current cash and cash equivalents balances, future cash flows expected to be generated from operating activities, available borrowings under its $175.0 million revolving credit facility and $250.0 million term loan facility will be sufficient to finance its current operations and obligations, and fund expansion of the business for the foreseeable future.

The Company settled its obligations under the Rollins, Inc. Pension Plan in 2019 without making any additional contributions during the years ended December 31, 2019 or 2018. The plan was fully funded with a prepaid balance. The plan assets exceeded the plan benefit obligations, and $31.8 million remained after settlement. The Company sold illiquid benefit plan asset investments during 2020 and used $18.0 million and $11.0 million of the $31.8 million during the years ended December 31, 2020 and 2019, respectively, to fund its 401(k) match obligations. As of December 31, 2020, the Company had approximately $1.2 million remaining of benefit plan assets which will likely be reverted to the Company per ERISA regulations in 2021.

The Company has one remaining pension in one of its wholly-owned subsidiaries. An employer contribution of $0.1 million was made during the year ended December 31, 2019. No contributions were made during 2020 or 2018. While the Company’s management does not expect to make a contribution to its remaining pension plan during fiscal year 2021, additional plan contributions, if any, will not have a material effect on the Company’s financial position, results of operations or liquidity.

Cash Used in Investing Activities

The Company used $162.4 million in investing activities for the year ended December 31, 2020, compared to $455.1 million and $101.4 million during 2019 and 2018, respectively. The Company invested approximately $23.2 million in capital expenditures during 2020 compared to $27.1 million and $27.2 million during 2019 and 2018, respectively. Capital expenditures for the year consisted primarily of property purchases, equipment replacements and technology-related projects. The Company expects to invest between $25.0 million and $30.0 million in 2021 in capital expenditures. During 2020, the Company and its subsidiaries acquired McCall Pest Management, Inc, the remaining Clark Pest Control locations, and Adam’s Pest Control in Australia as well as several other small to mid-sized companies for a total of $147.6 million compared to $430.6 million and $76.8 million in acquisitions during 2019 and 2018, respectively. The expenditures for the Company’s acquisitions were funded through existing cash balances, borrowings on our line of credit, a term loan, and other operating cash flows. The Company continues to seek new acquisitions.

Cash Used in or Provided by Financing Activities

The Company used $281.3 million in financing activities for the year ended December 31, 2020. During 2019, the Company generated $111.7 million from financing activities compared to using $175.4 million during 2018. The Company repaid $88.5 million of its outstanding debt balance throughout 2020, net of borrowings, compared to borrowing $291.5 million during 2019, net of repayments. A total of $160.5 million was paid in cash dividends ($0.33 per share) during the year ended December 31, 2020 including a special dividend paid in December 2020 of $0.09 per share, compared to $153.8 million in cash dividends paid ($0.31 per share) during the year ended December 31, 2019, including a special dividend paid in December 2019 of $0.03 per share and $152.7 million paid in cash dividends ($0.31 per share) during the year ended December 31, 2018, including a special dividend paid in December 2018 of $0.06 per share.

The Company reclassified certain prior period amounts in the Statement of Cash Flows from Operating Activities to Financing Activities for payment of contingent consideration to conform to the current period presentation.

| 21 |

The Company did not purchase shares on the open market during the years ended December 31, 2020, 2019 and 2018. There remain 11.4 million shares, adjusted for the December 10, 2020 three-for-two stock split, authorized to be repurchased under prior Board approval. The Company repurchased $8.3 million, $10.0 million, and $9.5 million of common stock for the years ended December 31, 2020, 2019 and 2018, respectively, from employees for the payment of taxes on vesting restricted shares.

The Company’s $98.5 million of total cash at December 31, 2020 is primarily cash held at various banking institutions. Approximately $71.3 million is held in cash accounts at international bank institutions and the remaining $27.2 million is primarily held in Federal Deposit Insurance Corporation (“FDIC”) insured non-interest-bearing accounts at various domestic banks which at times may exceed federally insured amounts.